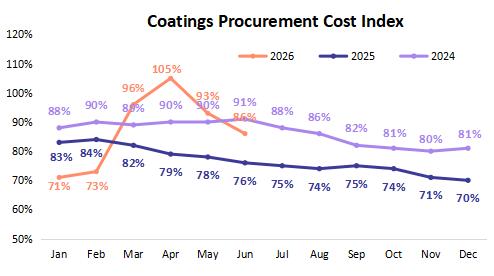

In June 2026, the domestic coatings and fine chemical raw materials market experienced "almost a full-scale decline." According to a comparison of data from the Chemical Plastic Research Institute between June and May, over 90% of chemical product prices dropped, with the coatings procurement cost index reaching 86% in June, a 7-point decrease month-on-month. Overall, midstream and downstream products such as coatings resins, curing agents, solvents, additives, and waterproof materials saw widespread month-on-month price declines, with most categories dropping by 5%-20%, while some high-end specialty raw materials fell by over 30%. In contrast, upstream basic raw materials in the titanium dioxide industry, such as sulfur and sulfuric acid, defied the trend and rose in price.

Top Decline: TMA Crash style Decline

Polyester resin raw materials for powder coatings have collectively fallen sharply, with TMA (trimellitic anhydride) experiencing the largest decline this month. The monthly average price plummeted sharply from 28842 yuan/ton in May to 16900 yuan/ton, with a single month drop of up to 41.41%; Next is TMP (trimethylolpropane), which plummeted 31.82% in June; Isobutyraldehyde and neopentyl glycol both experienced a decline of over 13%. The prices of high-end specialty raw materials have significantly decreased, and the two major curing agent industry chains of HAA and TGIC have simultaneously declined. The core raw materials of diethanolamine, adipic acid, and TGIC have all fallen by more than 11%. Coupled with the decline in epoxy chloropropane prices, the curing agent market lacks support.

Solvent: Ethylene glycol butyl ether, acetone, cliff descent

The solvent industry chain has also become one of the sectors with a significant decline this month. Ethylene glycol butyl ether plummeted by 22.67%; Acetone followed closely behind, plummeting 19.68% and approaching the integer level of 6000 yuan.

The collective decline in solvent products is directly related to the sharp decline in export orders from downstream industries such as coatings, inks, cleaning agents, and electronic chemicals. After the United States imposed tariffs, the export of downstream manufactured goods to the United States was hindered, and the consumption of solvents as "industrial MSG" was highly positively correlated with the manufacturing industry's prosperity. When terminal demand shrinks, the solvent process often bears the "first and deepest" pressure of price reduction. In addition, the prices of ethylene oxide and n-butanol, the raw materials for ethylene glycol butyl ether, have weakened simultaneously, resulting in reduced cost support.

Isocyanates: HDI and IPDI have fallen sharply, while TDI is relatively mild

HDI fell 14.28% this month; IPDI fell by 10.27%; TDI fell 6.70%. The core raw material of HDI, hexamethylenediamine, plummeted by 14.78%, and the monthly average price dropped from 26724 yuan/ton to 22775 yuan/ton, directly driving the rapid downward shift of HDI's cost center. The sharp decline in hexamethylenediamine is due to the oversupply caused by the concentrated release of adiponitrile production capacity. The decline in TDI is relatively small, and there is still some support in the domestic supply and demand pattern. However, if downstream exports of coatings and adhesives continue to be sluggish, TDI still has the risk of rebounding in the future.

Titanium dioxide industry chain: sulfur skyrockets, titanium dioxide slightly declines

The average price of rutile titanium dioxide in June only slightly decreased by 0.12% compared to May, basically maintaining a sideways trend. The price of upstream titanium concentrate has fallen synchronously, with a month on month decrease of 5.12%, and the raw material side has slightly benefited downstream. But 98% smelting sulfuric acid increased by 3.12% month on month, and solid sulfur surged by 16.35% in a single month, becoming one of the few price increasing categories in the entire industry chain.

Acrylic lotion/resin: conduction from upstream to downstream

Affected by the sharp drop of styrene, acrylate and lotion declined in an all-round way. Upstream styrene, acrylic acid, butyl acrylate and other monomers generally declined, of which styrene declined by 13.01%, and the collapse of the cost side directly drove down the price of lotion products.

As the core raw material of styrene acrylic lotion, the price collapse of styrene quickly transmitted to the end of lotion; While pure acrylic lotion uses acrylate as the main raw material, MMA (-2.49%) and butyl acrylate (-4.10%) have a relatively moderate decline, so the decline is small. MMA has shown some resilience in this round of decline, with relatively stable demand in downstream areas such as PMMA and light guide plates, playing a certain buffering role. However, whether the sharp drop in its raw material acetone (-19.68%) will be transmitted to MMA prices in the next 1-2 months needs to be continuously monitored.

Future prospects

Based on the current supply and demand pattern and cost trend, it is highly likely that the paint chemical raw material market will continue to fluctuate at a low level and operate weakly in July, with limited room for significant decline. July and August are in the seasonal off-season, and the downstream operating rate generally decreases under high temperature weather, making it difficult for the demand side to provide effective support in the short term. In the absence of demand pull, even if the cost side stabilizes, chemical prices may remain weakly volatile due to light trading. The trend of crude oil and commodities cannot be ignored. If international oil prices stabilize or rebound at the current level, it will provide cost support for downstream chemical products; If oil prices weaken further due to the expectation of a global economic recession, there is still room for a downward shift in the center of chemical prices.

(Note: All price data and indices in the article are quoted from the June 2026 market monitoring report of Buyi Plastics Research Institute. If you need to subscribe, Email:zhangq@ibuychem.com.)